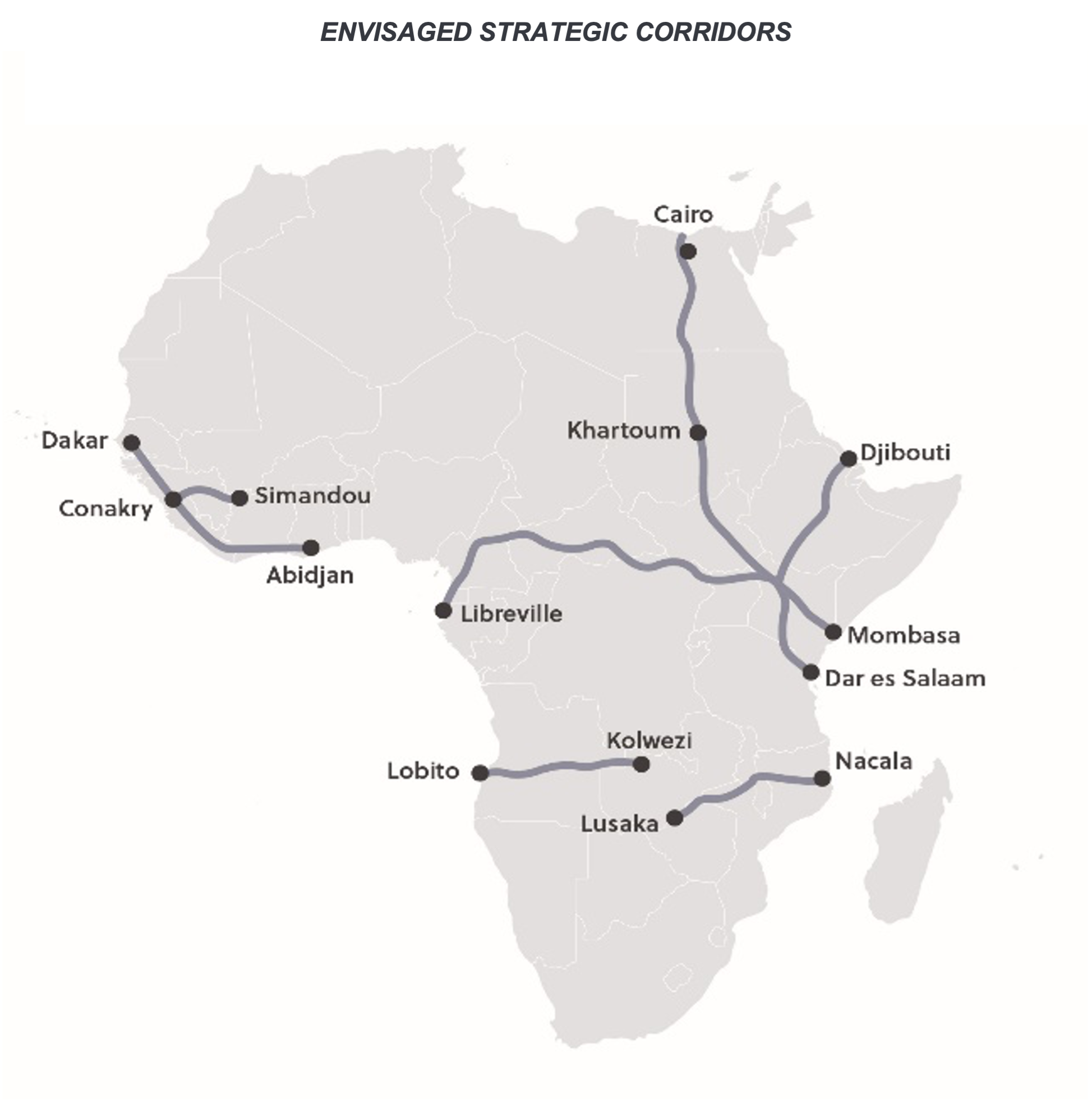

Beyond Lobito: Africa’s Strategic Corridors and the Future of Supply Chain Security

Report written by S-RM, our Strategic Intelligence Partner

Africa’s natural resources are in high demand as global powers race to shore up supply chains against a series of global shocks and geopolitical headwinds. Strategic logistics corridors – such as the flagship Lobito Corridor in Angola – have emerged as a secure and sustainable means to gain long-term access to these much-needed resources, in particular, critical minerals. Beyond Lobito, a new generation of multi-modal logistics systems are developing, from the Trans-Guinean railway connecting Guinea’s Simandou mine to port, to the rail system connecting Zambian mines to Mozambique’s Port of Nacala. These corridors are set to form the backbone of the supply chain for the energy transition, meeting at the convergence of the scramble for critical minerals, the hunt for new growth markets, and Africa’s push for regional trade and integration.

From ‘point projects’ to corridors

For years, investors have treated African infrastructure investment as a series of isolated bets: a pit here, a port there, a power plant bolted on later. That model is quietly being retired, as today’s flagship deals are increasingly structured around corridors – integrated systems where rail, ports, power, special economic zones, and regulatory frameworks are designed as a single package. This approach does more than bring efficiency to mineral exportation, it offers alternative revenue streams and lowers risk by anchoring long-lived assets to diversified economic activity in mining, agriculture, real estate and industry.

These projects also align with the direction that global supply chains are heading. As resource buyers seek alternatives to politically contested, sanctions-exposed, and tariff-burdened supply bases, Africa’s resource-rich hinterlands – and the long-haul infrastructure required to unlock them – is becoming a strategic priority. For this reason, global powers and multinationals still reeling from pandemic disruptions, sanctions and trade-wars now see these projects less as development philanthropy and more as insurance policies for future production.

Simandou: from blueprint to reality

No project captures this shift better than Simandou in Guinea. After nearly three decades of false starts, political disputes and licence revocations, the world-class high-grade iron ore deposit finally entered production in late 2025. The first commercial shipments, reaching Chinese ports just this month, are the visible tip of a $20 billion system of mines, a 650 kilometre railway, and a deep-water Atlantic Ocean port, built across difficult terrain. At scale, Simandou has the potential to supply about 120 million tonnes a year of premium ore, challenging incumbents in Australia and Brazil and lowering the emissions profile of steelmaking.

Simandou’s deeper significance lies not just in volumes but in governance. Western and Chinese-based consortia are co-developing a single integrated mine-rail-port system rather than rival lines, turning investors from simple offtakers into long-term operators and standard-setters in regional development. That model could be replicated as other corridors move from boardroom vision to project finance. On the opposite side of the continent, Japan’s decision to mobilise $7 billion for the Nacala Logistics Corridor – connecting resource-rich regions of Mozambique, Malawi and Zambia – underlines how G7 powers now see African routes as critical to securing transition minerals such as copper, cobalt, rutile and graphite.

A hinge for regional integration

The corridors are also a practical test for the African Continental Free Trade Area (AfCFTA), which aims to connect a 1.2 billion person, $2.5 trillion market but remains hostage to clogged borders and weak links between hinterlands and ports. The World Bank estimates that AfCFTA could add $450 billion to the continent’s income by 2035 and boost intra-African trade by more than 80 percent – but only if physical bottlenecks are removed. Policymakers increasingly describe these mine-anchored transport networks as “dynamic arteries” that turn tariff cuts into actual trade flows, often corridor by corridor rather than in one continental sweep.

By design, such projects necessitate cross-border collaboration on customs, transit rules and shared management of infrastructure. Nacala’s tripartite framework between Mozambique, Malawi and Zambia, and its planned links into the Democratic Republic of Congo, illustrate how corridor governance can deepen regional integration while remaining grounded in tangible assets and freight volumes. For investors, this promises access to long-dated, often dollar-linked cash flows underpinned by sovereign and multilateral backing, and the chance to build platforms for follow-on deals in logistics, energy, and real-estate along the way.

Competing for influence

The corridors have become core terrain in the contest between China, the US, Europe and Gulf states – a key dynamic that will continue to shape the investment landscape. While Beijing has had an almost two decades-long headstart by tying infrastructure finance to mineral offtaking deals, Washington is catching up quickly, using the Lobito Corridor as a test case for securing non-Chinese supply chains for copper and cobalt. The European Union has also codified its strategy through the Global Gateway plan, which targets €300 billion in global corridor development, with almost half of that slated for Africa. Meanwhile, Gulf actors such as DP World and AD Ports are assembling their own ports-and-corridors strategy, stringing together concessions from Berbera and Djibouti to Mombasa, Dar es Salaam and Pointe-Noire to channel East African trade towards Gulf hubs.

But the story is not purely zero-sum. Simandou’s joint development shows that competitive coexistence – even reluctant cooperation – is possible when geology and geography favour a single route.

Final word: The fine print on risk

For investors willing to engage early, Africa’s strategic corridors offer a rare alignment of strong growth fundamentals, structural demand, and the ability to package multiple, de-risked revenue streams into one package. Anchor assets – mining licences, rail and port concessions, industrial parks and logistics hubs – provide entry points into ecosystems that can support everything from power and pipelines to housing, retail and professional services. There are also genuine environmental and social upsides: shifting bulk cargo from trucks to rail cuts emissions and accidents, while corridor-linked processing can create jobs and help host governments build sovereign wealth funds and human capital.

But these projects need to be managed for risk. Political instability and regulatory volatility have derailed grand plans, as Simandou’s own history of licence disputes and renegotiations attests. Entrenched patronage networks, from politically connected contractors in Nacala to the government’s preferred construction firm in Lobito, raise corruption and reputational risks across the corridor supply chain. For long-term capital the implication is clear: success will depend less on smart financial engineering than on building durable partnerships with host governments and communities, and accepting that risk management strategies are just as valuable as the ore at the end of the line.